Introduction to Economics

Welcome to my introduction lesson, where I hope you will gain a basic understanding of the fundamental concepts.

Objectives:

I can explain how scarcity impacts opportunity costs

I can analyze how governments react to scarcity by reviewing their answers to the three basic economic questions of What, How, and For Whom.

I can differentiate economic systems by creating a graphic organizer based off from how governments react to scarcity and match up the proper economists to the correct system

GOAL:

All students will demonstrate their knowledge of scarcity and other fundamental concepts by summarizing and demonstrating their understanding by on the Unit 1 assessment by achieving a 70% or higher.

STANDARDS

SS.E.1.1.1 Scarcity, Choice, Opportunity Costs, and Comparative Advantage - Using examples, explain how scarcity, choice, opportunity costs affect decisions that households, businesses, and governments make in the market place and explain how comparative advantage creates gains from trade.

SS.E.1.4.4 Functions of Government - Explain the various functions of government in a market economy including the provision of public goods and services, the creation of currency, the establishment of property rights, the enforcement of contracts, correcting for externalities and market failures, the redistribution of income and wealth, regulation of labor (e.g., minimum wage, child labor, working conditions), and the promotion of economic growth and security.

SS.E.3.1.1 Major Economic Systems - Give examples of and analyze the strengths and weaknesses of major economic systems (command, market and mixed), including their philosophical and historical foundations (e.g., Marx and the Communist Manifesto, Adam Smith and the Wealth of Nations). (National Geography Standard 11, p. 206)

TASK #1

What is the fundamental problem of economics?

Consider the following scenario.

Imagine that you walk into a classroom and immediately notice there are far more students than there are desks and your teacher tells you that you must find as a solution as a class. You must decide who gets them, who will not and why.

This scenario represents the fundamental problem in economics, watch the following video clip to learn more about it.

*Use this note outline to learn guide your attention while watching the video.

TASK 1 video notesHere is a link to the video just in case the video doesn't load

What is the fundamental problem of economics?

After watching the video clip answer the review questions on quizizz

*If you did not answer 2 of the 3 questions correctly review your notes attempt the questions again, and then visit this clip from Mr. Clifford as he explains the economic concept using Star Wars as an example.

Here is a link to the video just in case the video doesn't load

TASK #2 OPPORTUNITY COST

Congratulations, now that you know what SCARCITY is, let’s analyze economic decision making.

The next major economic concept you will be investigating is something you have been doing most of your life, deciding what to do with your time, money, or energy because you cannot be in two places at one time.

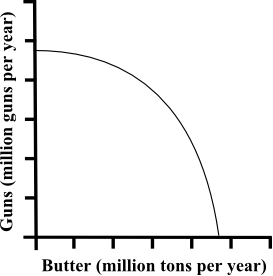

The most common example used in economics to analyze a country’s production options is a Production Possibilities Curve, as it illustrates Opportunity Cost.

Consider these two options, our country can use our all of limited resources to produce just GUNS or just BUTTER or a combination of both. A Production possibilities Curve illustrates the opportunity cost (or the cost of the next best alternative we cannot have) GUNS or BUTTER. Take a look at the example below

Opportunity Cost

Watch the following video clip that uses the movie Monster’s Inc. to learn about how Producers (Businesses) deal with these economic limitations.

Economovies Opportunity Cost in Monster's Inc

?Still don't get it, here is a link to deeper look into What Opportunity Cost is and how it is graphed.

?Still don't get it, here is a link to deeper look into What Opportunity Cost is and how it is graphed.

Here is a link to the video just in case the video doesn't load

https://www.youtube.com/watch?v=kmjzgB_tUJ8

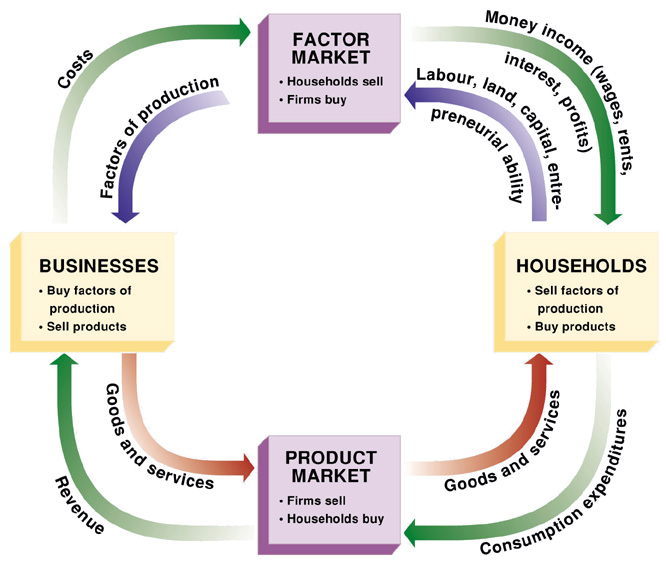

TASK #3 The Factors of Production, the Circular Flow Model, and the Lorax

Welcome to Task #3 where you will analyze the factors of production, interpret the circular flow model of economics, and then apply what you have just learned to where it appears in The Lorax.

What are the factors of Production

1.

2.

3.

4.

This chart illustrates the interactions between households and businesses in the factory market (think factories) and the product market (think Target).

Factor Markets- are where the factors of production are bought and sold

Product Markets- where consumer goods are available to buy

*Consumers exchange their money in the product market and come home with the goods they purchased.

*Households supply the labor to the businesses in the factor markets as they manufacture goods in exchange for wages.

*Households supply the labor to the businesses in the factor markets as they manufacture goods in exchange for wages.

Check for understanding. Take the quiz to test your knowledge.

Quizizz Code: 222735

Now let's apply what you know about the factors of production and the circular flow chart in applying what you know to the video The Lorax

Directions:

Watch the Lorax (25 minutes) and answer the guiding questions in the viewing guide to apply what you know about the Factors of Production and the Circular flow model to the Lorax.

Here is a link to the video just in case the video doesn't load

https://www.youtube.com/watch?v=8V06ZOQuo0k

Answer the guiding questions about the Lorax (you will find them in Task #3 of your notes organizer).

TASK #4 What economic system best suits your needs?

Now that you know that scarcity forces all of us into opportunity costs (the cost of the alternative not chosen) lets take a look how these same decisions lead to different economic systems.

Directions:

https://www.youtube.com/watch?v=B43YEW2FvDs

Directions:

Watch this video clip to learn more about the 4 major economic systems

Command

Traditional

Mixed

Market

Watch the video clip to learn about the four types of economic systems, you must be able to answer these three questions for each system

Who decides what to produce?

Who makes the decision of how to produce it?

Who decides access to the resources/goods?

https://www.youtube.com/watch?v=B43YEW2FvDs

Finally read about the 3 major economists Adam Smith, Karl Marx, and John Maynard Keynes and then match them up with the economic systems (exclude Traditional Econ in this task).

This chart should help you match up countries to economic systems

Check for understanding:

Next complete the graphic organizer to compare/contrast the economic systems and then match up the appropriate country to the proper system. (YOU WILL FIND THIS ACTIVITY IN YOUR NOTES)

Assessment

*NOW IT IS TIME TO TEST WHAT YOU HAVE LEARNED.

Follow this link and complete the assessment

Quizizz Code: 797219

Resources

1. Scarcity

https://www.youtube.com/watch?v=1cYMW5d_bn4

2. Opportunity Cost

https://www.youtube.com/watch?v=kmjzgB_tUJ8

Mr. Jacob Clifford Economovie clips

1. Scarcity

2. Opportunity Cost

https://www.youtube.com/watch?v=tW4G5IPpzFY&spfreload=5

3. Crash Course Economics

https://www.youtube.com/watch?v=B43YEW2FvDs

Chegg Study

1. PPC Graph

http://www.chegg.com/homework-help/definitions/production-possibilities-curve-ppc-12

Spectrum of Economic Systems

1. http://images.slideplayer.com/14/4253238/slides/slide_6.jpg

No comments:

Post a Comment